A new report published today by the Tax Justice Network, focuses on the role that corporate registries in the European member states play in fighting fiscal fraud and tax avoidance. The report presents results from a new survey sent out by the Tax Justice Network to corporate registries of all European member states. It analyses the data we received from seven respondent jurisdictions (the UK, Sweden, Denmark, Romania, Belgium, Latvia, Slovenia and Slovakia) and combines it with additional data available through the International Business Registers reports and the Financial Secrecy Index.

While nobody would dispute the important contributions corporations make towards a prosperous society, strong evidence from several offshore leaks disclosed in recent years highlights the immense risks that arise when corporations are afforded significant levels of both power and secrecy. The amount and quality of information available to authorities and the public about corporate vehicles is often the decisive factor that tips the balance between the usefulness and harmfulness of corporations. Given that corporate registries constitute the primary source of information about a corporate entity for the public as well as for authorities like financial crime investigation units and tax administrations, corporate registries play an important role in preventing corporations from being misused to conceal money laundering, tax evasion and corruption – all of which foster inequality within and often in between countries.

We designed the survey to assess the legal powers and capacities of corporate registries. The survey is also designed to look for variables that could indicate whether corporates registered in a particular jurisdiction are more likely to be used for illicit purposes. General indicators included:

- “Attractiveness” of a jurisdiction’s company law

- Transparency regarding the natural persons involved with registered companies

- Transparency of registered companies’ business

- Corporate registries’ budgets and staff sizes

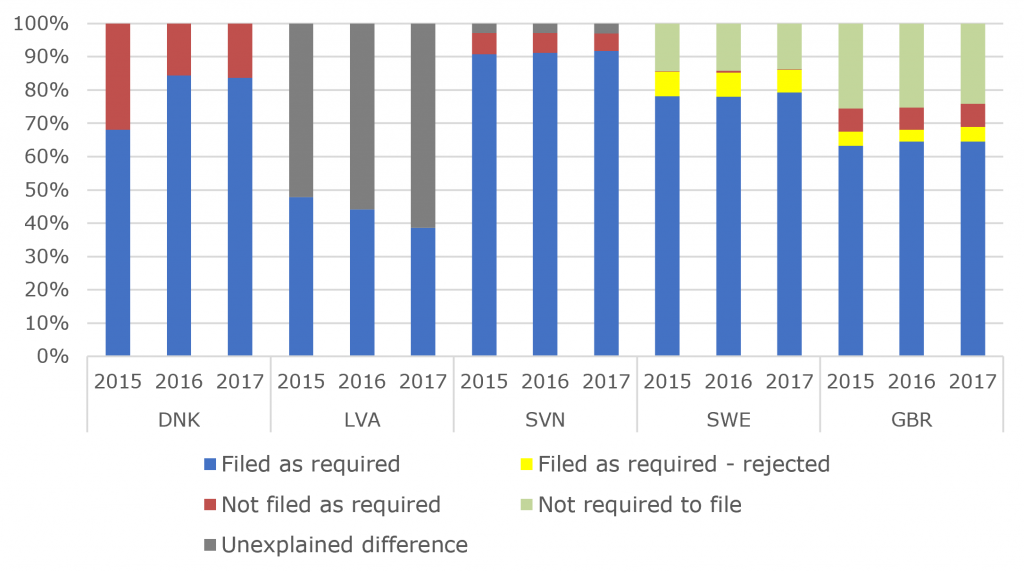

Some of the indicators we assessed may require further research due to the response rate and the concern that the sample analysis may not be representative for all jurisdictions. Nonetheless, the report presents some interesting findings. As the chart underneath illustrates, we found that 32 per cent of the limited companies in Denmark did not file accounts as required by law and approximately 250,000 limited companies in the UK failed to file their accounts as well. That may indicate a problem with the de facto availability of annual accounts.

Figure: Filing of annual accounts by limited companies as percentage of total number of registered limited companies

Both Belgium and the UK reported a high number of companies that dissolved within a year of incorporation and may have thus never been required to file their accounts. It should be investigated whether this practice is frequently used for illicit financial activity. Furthermore, about 500,000 limited companies in the UK were considered dormant. This may pose a risk given that dormant companies only need to file an abbreviated version of accounts.

Three respondent countries permit foreign companies to operate within their jurisdictions without registering. This might enable individuals to circumvent domestic laws and register in another jurisdiction which offers weaker regulation.

Finally, regarding identification of beneficial owners, we found that jurisdictions employ only a few data validation activities such as cross-checking with other registries or allowing anonymous reporting of false information. We recently published another report on the verification of beneficial ownership available here.

Today’s report is the second of a twin project, funded by the European Union Horizon 2020 as part of the Combating Fiscal Fraud and Empowering Regulators (COFFERS) programme. The twin project aims to generate comprehensive comparative analyses of administrative and enforcement capacity of both tax administrations and corporate registries in European member states, to counter fiscal fraud and tax avoidance. The first part of the project focused on the capacity of tax administrations in the European Union to fight inequality and was published by the Tax Justice Network on 15 November 2018.

The author

Related articles

UN tax convention hub – updates & resources

A heartfelt farewell to our dear Óscar

Public finance is feminist terrain

New Tax Justice Network reports on real estate transparency

Beneficial Ownership of Real Estate Around the World

7 July 2026

Integrating the Collection, Use and Exchange of Real Estate Ownership Information

7 July 2026

Four definitions to change the world: Struggles over meaning in the UN tax convention negotiations

Fiscal hell or mirage? What Spain’s wage debate gets wrong

Introducing the Real Estate Secrecy Index

Indicator deep dive: Golden Visas