Moran Harari ■ New report on European tax administrations’ capacity in preventing fiscal fraud and tax avoidance

The Tax Justice Network released today a report on the capacity of tax administrations in the European Union to fight inequality by combating fiscal fraud and tax avoidance. The report analyses the results of a survey consisting of 71 questions that was sent by the Tax Justice Network to the tax administrations of all EU Member States. It explores the data we received from seven respondent jurisdictions and combines it with additional data available through the International Survey on Revenue Administration (ISORA). A condensed version of this report has been presented by Frederik Heitmüller on 2 November 2018 at the CESifo Economic Studies Conference on New Perspectives on Tax Administration Research.

In recent years, there have been several initiatives to assess the capacity of tax administration by international organisations and other bodies. These include the Revenue Administration Fiscal Information Tool (RA-FIT) by the IMF, the Fiscal Blueprints by the European Union and the Tax Administration Diagnostic Assessment Tool (TADAT) by the IMF. However, these initiatives are all either limited in scope, in continuance, or in transparency. The ISORA report, a collaboration between the OECD, the Inter-American Centre of Tax Administration (CIAT), the Intra-European Organisation of Tax Administrations (IOTA) and the IMF, is to date the most comprehensive available database of tax administrations by far. Nonetheless, there are still many data gaps in the evaluation of the capacity of tax administrations and there is currently no mapping available on the published statistics or public datasets by national tax administrations.

One of the reasons for these gaps is likely to be the sensitive nature and confidentiality of the data involved. As tax is directly related to the core of statehood and sovereignty, it is often jealously guarded, and some jurisdictions may be unwilling to share data that may reveal shortcomings in sensitive functions of tax administration. Furthermore, to our knowledge, specific issues that are relevant to inequality have not been assessed in any of the reviewed surveys.

This report published today attempts to close this gap.

The report focuses on several topics that address data gaps we identified in the available datasets on capacity of tax administrations. Based on the analysis of the data, we identify the most critical challenges tax administrations face in countering inequality. These are predominantly:

- Performance and staffing of large taxpayer offices

- Protection of whistleblowers

- Audits and prosecution activities

- The “revolving door” phenomenon.

While the data provided by the seven jurisdictions may not be sufficient to draw final conclusions about the capacity of all EU tax administrations, it provides an indication about which hypotheses are worth pursuing more in-depth in future research.

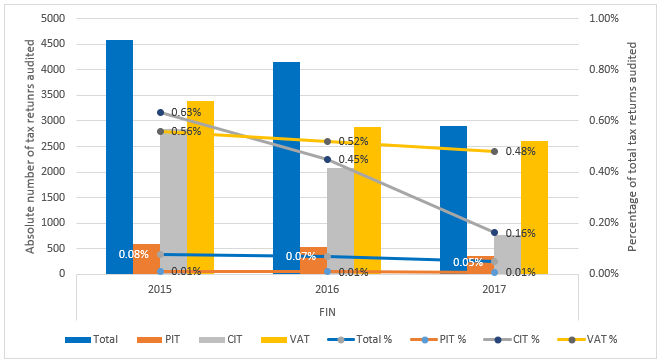

For example, an interesting finding relates to the scale of audit activity. We looked at the number of tax returns tax administrations have audited between 2015 and 2017, checking separately for corporate income tax, personal income tax and VAT. What we found is a decline in the practice of auditing tax returns, predominantly with regard to tax returns of corporations, as well as a decline in the number of on-site audits in two out of three countries that responded to that question. Further research should investigate how this decline can be explained. Potential hypotheses include lower budgets or political interference, but also a greater reliance on IT and data analysis solutions or pre-populated tax returns.

Number of audits of tax returns – Finland

This is the analysis of data by Finland, but a similar trend was seen for other countries.

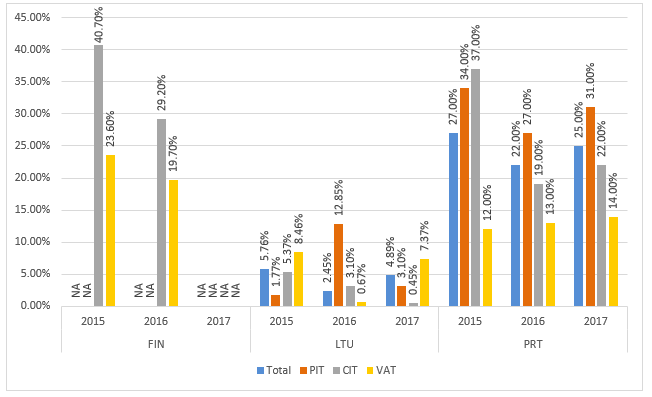

We also revealed that the effective collection of penalties seems to be a problematic issue, as none of the jurisdictions that reported data succeeded in collecting more than 50 per cent of the penalties that were charged in any of the years. Further research could explore what stands in the way of an effective collection of penalties, whether administrations lack the capacity to collect or whether there may be more political reasons for a lack of enforcement.

Percentage of number of administrative penalties collected so far

The analysis of all the data we received as a response to our survey can be downloaded here.

Tax laws, progressive as they may be, may become toothless and even regressive if they are not properly enforced. The report emphasises the importance of conducting further studies and assessing whether the legal tools are effectively used by tax administrations to combat fiscal fraud and tax avoidance.

Today’s report is the first from a twin project, funded by the European Union Horizon 2020 as part of the Combating Fiscal Fraud and Empowering Regulators (COFFERS) programme. The twin project aims to generate a comprehensive comparative analysis of administrative and enforcement capacity of tax administrations and corporate registries in European member states, to counter fiscal fraud and tax avoidance. We will publish the second part, which focuses on corporate registries, in a few weeks.

The author

Related articles

The bitter taste of tax dodging: Starbucks’ ‘Swiss swindle’

The tax justice stories that defined 2025

Admin Data for Tax Justice: A New Global Initiative Advancing the Use of Administrative Data for Tax Research

")

2025: The year tax justice became part of the world’s problem-solving infrastructure

‘Illicit financial flows as a definition is the elephant in the room’ — India at the UN tax negotiations

Tackling Profit Shifting in the Oil and Gas Sector for a Just Transition

The State of Tax Justice 2025

The “millionaire exodus” visualised

The millionaire exodus myth

10 June 2025