Nick Shaxson ■ Do real investors chase corporate tax cuts?

Guess which one got the corporate tax cut?

Cross-posted with Fools’ Gold.

From the Financial Times, a report on a survey by the Tolley Tax Journal of businesses’ responses to the UK’s policy of savage cuts to the corporate income tax. It’s about the UK, but it has wide international relevance.

“More than six out of 10 respondents thought the cut in the corporate tax rate, by 8 percentage points to 20 per cent, had boosted their own companies’ investment and growth, although for most it only had a marginal impact.”

Our emphasis added. Asking corporate bosses whether they think corporate tax cuts are a good idea is a bit like asking children to assess whether a policy of handing out free sweets is a good idea. These things don’t necessarily even help corporations much: as we’ve noted before, such tax cuts can be like refined sugar in the human body: empty financial calories with adverse long-term health effects.

That corporates are damning this gargantuan giveaway by UK businesses with such faint praise should be taken as an indictment of the tax-cutting policy.

“As a businessman I never made an investment decision based on the tax code… if you are giving money away I will take it. If you want to give me inducements for something I am going to do anyway, I will take it. But good business people do not do things because of inducements.”– Paul O’Neill, former head of Alcoa and ex U.S. Treasury Secretary under George W. Bush.

This feast of corporate tax-cutting has been touted by the government, and many others who haven’t thought very hard about the issues, as a ‘competitive’ tax policy for the country. But this is pure woolly thinking, for many reasons.

For one thing, as has recently been pointed out, the cut in the headline corporate tax rate from 28 to 20 percent has cost the UK government some £7 billion in annual corporate tax revenue. That is around six times the entire annual expenditure of Oxford University.

How is this equation supposed to make the UK economy more “competitive?” We have been asking versions of this question for many years now – and we have never heard a satisfactory response.

The inset quote from Paul O’Neill highlights another reason why corporate tax cutting has such a poor record of fostering economic growth and other good things: they are like pushing on a string, even in the best of times.

If you don’t believe us, then take a look at the generic reasons why corporate tax-cutting is unlikely to make anyone’s economy more ‘competitive’ – and then see if you can rebut any of them. Or, if you have more time, get your head around this longer document, entitled Ten Reasons to Support the Corporate Income Tax.

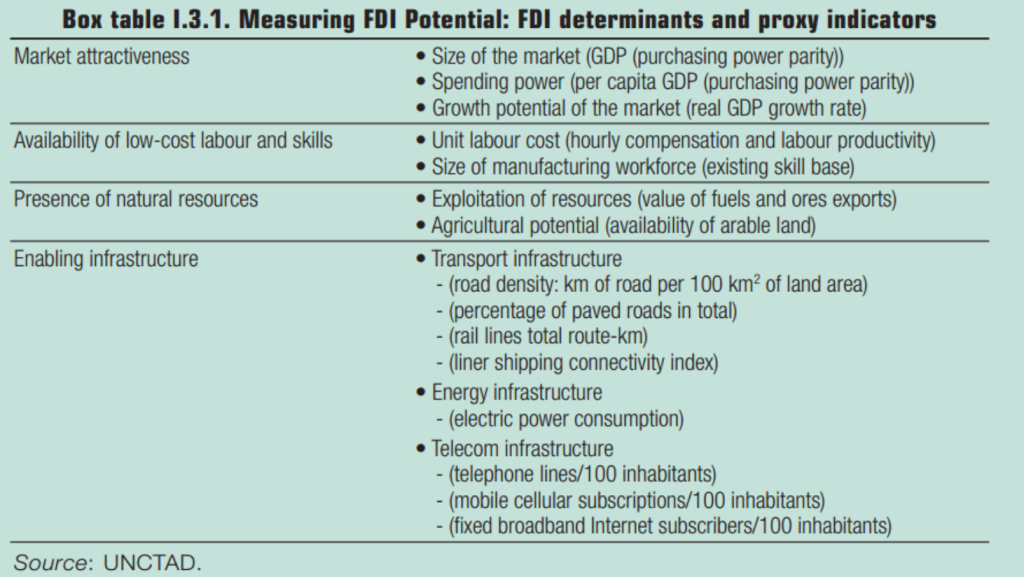

Now here is a fresh piece of information, in support of just one of those reasons. It comes from UNCTAD (p30), which has published “FDI Attraction and Potential Indices” in its annual World Investment Report since 2002. These indices, which look at the factors that affect real Foreign Direct Investment, have hardly changed since then.

Note that among these factors, there is a three-letter word ending in -x that is missing. And that’s for good reason. Corporate taxes are not costs to an economy but a transfer within them, from one wealth-creating sector to another.

There is no a priori reason why such a transfer should make an economy as a whole more ‘competitive.’

Endnote: the FT cited story did say that corporations were more interested in investment allowances than in headline corporation tax cuts. But that’s another story, for another day.

The author

Related articles

🔴Live: UN tax negotiations

Just Transition and Human Rights: Response to the call for input by the Office of the UN High Commissioner for Human Rights

13 January 2025

Tax Justice transformational moments of 2024

The Tax Justice Network’s most read pieces of 2024

Breaking the silos of tax and climate: climate tax policy under the UN Framework Convention on International Tax Cooperation.

Seven principles of good taxation for climate finance

9 December 2024

Joint statement: It’s time for the OECD to walk the talk on human rights

Did we really end offshore tax evasion?

The State of Tax Justice 2024

EU public consultation on the Anti-Avoidance Directive